Why do so many stores have the new chipped credit card terminals but they still aren’t working?

This question was answered on April 6, 2016. Much of the information contained herein may have changed since posting.

The United States is the last major market in the world to transition away from the less secure magnetic swipe process to the much more secure chip readers.

The United States is the last major market in the world to transition away from the less secure magnetic swipe process to the much more secure chip readers.

Even though the U.S. only accounts for roughly a quarter of all credit card transactions, we’re responsible for about 50% of fraud worldwide because we still use the magnetic swipe process.

Anyone that has a newer ‘chipped’ EMV compliant credit card knows how uncommon it is to actually be able to use it.

Some industry reports estimate that 4 out of 5 chipped terminals that are installed are still not able to accept chipped cards.

Even though the credit card industry mandated retailers convert their processing equipment last October or face higher liability for fraudulent transactions, the complexity of the transition is much greater than simply placing a new terminal at the counter.

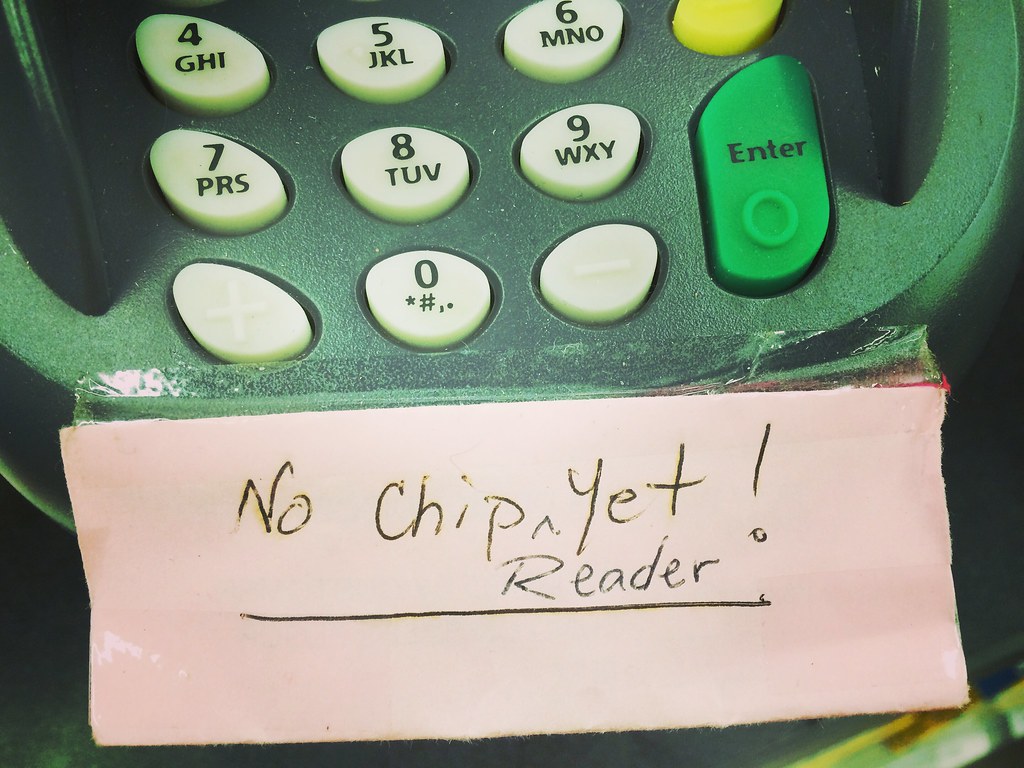

The hardware portion of the conversion is what you’re typically seeing at retailers - mostly with signs saying “chip reader has not been activated” taped over the card slot.

The expense of replacing credit card terminals, especially for smaller retailers, was thought to be the initial cause of the delay, but since we’re seeing so many non-functioning terminals, we’re well past that excuse.

One of the biggest reasons the new chipped terminals aren’t working for so many retailers is not the hardware, but the software required to integrate the terminals into the point-of-sale and back office processes.

Generally speaking, retailers are at the mercy of their software vendors to get the updated process implemented and the more complex the existing system, the longer it may take.

You may have noticed that small ‘mom & pop’ shops that use services such as Square have already converted because they’re using a standardized system that is much less complicated.

Custom point-of-sale software has to be certified by each of the credit card companies and associated merchant banks in order to be compliant and the backup in getting certified is one of the many contributors to the delay.

Another contributing factor is how debit cards are processed, which is different than credit cards adding to the complexity of updating the software.

Some companies may have the credit card portion of the equation figured out, but are waiting to get the debit card processing finalized before rolling out the updates.

If they didn’t wait, imagine the potential confusion when trying to use a chipped credit card vs. using a chipped debit card – one would work, but the other wouldn’t.

To add to the fun, there’s still one more transition waiting in the wings.

Today’s chip and sign process still allows for fraud because there is no verification of the signature (you can sign as Mickey Mouse and no one will generally notice).

The ultimate security will be in place when we all use our chipped cards with an associated PIN, but the complexity and expense of implementing that system is even greater, so we’re a long way from the finish line on chipped card processing.

(Image courtesy of https://www.flickr.com/photos/stevendepolo)

About the author

Posted by Ken Colburn of Data Doctors on April 6, 2016

Need Help with this Issue?

We help people with technology! It's what we do.

Contact or Schedule an Appointment with a location for help!

Free Help

Articles & Advice

Video News

Newsletter

Approved Software

Ask a Question

855-328-2362

Newsletter

Sign up for our newsletter and get free tips and tricks to keep your computer running great!